As I discussed in a prior post (here), in March 2014 the U.S. Supreme Court agreed to take up the IndyMac case in order to consider whether the filing of a class action lawsuit tolls the statute of repose under the Securities Act (by operation of so-called “American Pipe” tolling) or whether the statute of repose operates as an absolute bar that cannot be tolled. The case will be heard during the next Supreme Court term. In the following guest post, Stanford Law School Professor David Engstrom, who filed an amicus brief in the case, takes a look at the IndyMac case and its implications for class action securities litigation.

As I discussed in a prior post (here), in March 2014 the U.S. Supreme Court agreed to take up the IndyMac case in order to consider whether the filing of a class action lawsuit tolls the statute of repose under the Securities Act (by operation of so-called “American Pipe” tolling) or whether the statute of repose operates as an absolute bar that cannot be tolled. The case will be heard during the next Supreme Court term. In the following guest post, Stanford Law School Professor David Engstrom, who filed an amicus brief in the case, takes a look at the IndyMac case and its implications for class action securities litigation.

I would like to thank Professor Engstrom for his willingness to publish his article on this site. I welcome guest post contributions from responsible authors on topics of interest to readers of this blog. Please contact me directly if you would like to submit a guest post. Here is Professor Engstrom’s guest post:

****************************

The Supreme Court has granted certiorari in Public Employees’ Retirement System of Mississippi v. IndyMac MBS, Inc., a case that has significant implications for securities class actions and the efficient operation of the federal courts. I recently filed an amicus brief in the case with eleven academic colleagues (found here)[1] using data from Stanford Securities Litigation Analytics.[2] The brief assists the Court by showing that, if the Second Circuit’s decision below were to stand, class members in a large number of securities class actions would have to make wasteful “protective filings” in order to maintain their right to proceed independently and avoid being time-barred if class certification was subsequently denied. These filings would drain judicial resources and impose costs on putative class members without any countervailing benefit.

In American Pipe & Construction Co. v. Utah, 414 U.S. 538 (1974), the Supreme Court held that the filing of a class action complaint “suspends the applicable statute of limitations as to all asserted members of the class who would have been parties had the suit been permitted to continue as a class action.” Id. at 554. A contrary rule, the Court warned, would impair the “efficiency and economy of litigation.” Id. at 553. In its IndyMac decision below, the Second Circuit broke with this proposition, refusing to apply American Pipe’s tolling rule to the three-year limitations period in Section 13 of the Securities Act in a case brought under Sections 11 and 12 of the Securities Act, which address misstatements and omissions of material information related to a public offering. Under the Second Circuit’s rule, a putative class member must thus file a protective action—either intervening in the class action or filing entirely separate suits—on the eve of expiration of Section 13’s three-year limitations period in order to preserve the right to proceed independently if class certification is later denied.

An important question in this case, as the Second Circuit noted, is the quantity of protective filings that can be expected if American Pipe does not apply to Section 13’s three-year limitations period in Section 11 and 12 cases. A related question not addressed in this case, but clearly implicated, is the number of protective filings we can expect if the Second Circuit’s holding is extended to the similar five-year statute of limitations applicable to the much larger number of securities class actions brought under Section 10(b) of the Securities Exchange Act.

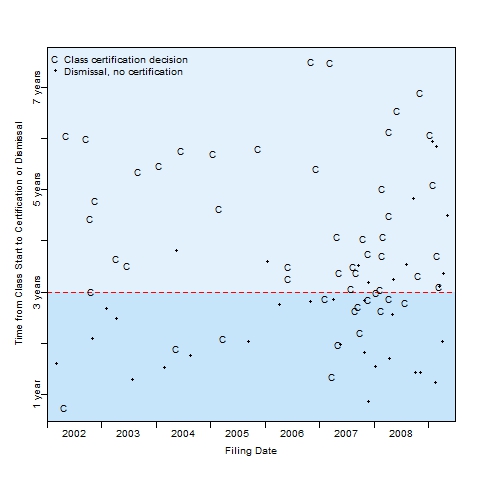

Data on class actions filed during 2002-2009 helped answer these questions. We first estimated the proportion of cases asserting only Section 11 and 12 claims in which a class certification order occurred after Section 13’s three-year limitations period had expired. More specifically, we calculated the number of days between the first day of the class period and either: (i) the date of the district court’s order on a motion for certification (or, in multi-certification-order cases, the last certification order); or (ii) the date of the district court’s order preliminarily certifying a class for purposes of settlement.[3] The results of these calculations are presented in Figure 1’s scatterplot.

Figure 1. Time from the Start of the Class Period to a Certification Decision or a Dismissal Without Certification in Cases Asserting Only § 11 or 12 Claims, 2002-2009

The results are striking: Section 13’s three-year limitations period, denoted in Figure 1 as a horizontal dashed line, would have expired prior to a certification decision in 73 percent (38 of 52) of cases that reached a certification decision, and prior to a certification decision in 44 percent (38 of 86) of all filed cases. To provide more detail on the 52 cases depicted in Figure 1 that reached a certification decision, the three-year limitations period would have expired before an order on a free-standing motion for class certification in 11 of 12 cases reaching such an order. And that period would have expired in 29 of the 42 cases that reached certification as part of the court’s preliminary approval of a settlement.[4]

Figure 2 presents the results of the same analysis for cases brought under Section 10(b) of the Securities Exchange Act, which is governed by a five-year limitations period.[5] Data on these cases is taken from a random sample of 500 cases drawn from roughly 1,200 securities class actions filed between 2002 and 2009.[6] The results are again striking: The five-year limitations period that applies to § 10(b) claims would have expired prior to a certification decision in 44 percent (135 out of 307) of cases that reached a certification decision and prior to a certification decision in 27 percent (135 out of 500) of all cases in the sample.[7]

Figure 2. Time from the Start of the Class Period to a Certification Decision or a Dismissal Without Certification in Cases Asserting § 10(b) Claims, 2002-2009

Among the 307 cases in which class certification occurred, 227 classes were certified for the purposes of settlement, and 86 classes were certified in response to free-standing motions to certify. Of the 227 cases certified for settlement purposes, 97 came after the five-year limitations period; of the 86 cases producing an order upon a free-standing motion for certification, 42 came after the limitations period.[8]

Using the above estimates and extrapolating to the roughly 3,200 securities class actions filed since 1997 alleging either Section 11, 12 or 10(b) violations, plaintiffs seeking to preserve their rights without American Pipe’s protective rule would have had to make protective filings in as many as 850 cases.[1][9] Had even a handful of potential class members in each case done so as the end of the relevant three- or five-year limitations period approached, total filings would have easily numbered in the thousands.

Moreover, as we explained in our brief, these calculations may even underestimate the effect of the Second Circuit’s ruling. First, a significant number of cases are dismissed without certification after the limitations period expires. These cases—denoted as dots falling above the dashed line in Figures 1 and 2—could generate protective filings but are not included in the above estimates. Second, a potential class member’s rights can be cut off by the limitations period because of any defect that is fatal to a class claim, not just denial of certification. Without American Pipe’s protective rule, class members who lack confidence that the lead counsel has cleared all legal hurdles to recovery may make protective filings even after class certification has been granted. Third, if American Pipe’s protective rule does not apply, both lead counsel and defendants will have incentives to drag their heels in the course of pre-trial proceedings in order to cut off potential class members’ opt-out rights. Finally, the Court’s June 23rd decision in Halliburton strongly suggests that class certification proceedings will likely take longer going forward. This is because at least some cases will involve dueling expert opinions (including “event studies” using multiple-regression to measure stock-price movement at the time of a false or misleading statement) in order to determine whether the presumption of reliance on which federal securities law rests can be rebutted. Additional pre-certification proceedings of this sort will likely push more cases above the horizontal dashed lines in Figures 1 and 2, thus increasing the proportion of cases that could generate wasteful protective filings.

Procedure cases often entail difficult trade-offs – for instance, between speed and accuracy in weighing the merits of a case. In this case, however, there is no benefit to requiring potentially thousands of protective filings in securities class actions.

[1] Signatories other than me include: Janet Alexander, Stanford Law School; Stephen Burbank, Penn Law School; Kevin Clermont, Cornell Law School; John Coffee, Columbia Law School; James Cox, Duke Law School; Scott Dodson, Hastings Law School; Jonah Gelbach, Penn Law School; Alexandra Lahav, Connecticut Law School; David Marcus, University of Arizona Law School; Norman Spaulding, Stanford Law School; and Benjamin Spencer, Washington & Lee Law School.

[2]Stanford Securities Litigation Analytics, co-founded by Professor Michael Klausner and Jason Hegland, is a practitioner-focused research group with extensive databases covering securities class actions and SEC enforcement actions. They are launching a new web tool for practitioners that will allow detailed queries of the database, aggregated statistics based on search results and interactive data visualizations.

[3] Keying this calculation to the start of the class period is consistent with § 13’s language, which states that the limitations period begins to run when the security was “bona fide offered to the public” (§§ 11 and 12(a)(1) claims) or upon the security’s “sale” (§ 12(a)(2) claims).

[4] Two of the cases in the sample of §§ 11 and 12 cases produced both an order on a motion for certification and a preliminary order approving a class settlement beyond the three-year limitations period, which explains why the numbers reported for cases falling into each category sum to 40 (11 + 29) rather than 38.

[5] See 28 U.S.C. § 1658(b) (requiring securities fraud cases brought under § 10(b) and Rule 10b-5 to be brought within “5 years after such violation”).

[6] As with the prior analysis, keying the calculation of elapsed time to the start of the class period is consistent with the weight of authority among lower courts that § 1658(b)’s five-year limitations period is subject to an event-accrual rule – i.e., the date of the misrepresentation or the completion of (or commitment to complete) the purchase or sale of the security. See, e.g., McCann v. Hy-Vee, Inc., 663 F.3d 926, 932 (7th Cir. 2011) (holding that the five-year limitations period starts upon misrepresentation); In re Exxon Mobil Corp. Sec. Litig., 500 F.3d 189, 200 (3d Cir. 2007) (same); see also Arnold v. KPMG LLP, 334 Fed. App’x 349, 351 (2d Cir. 2009) (explaining that the limitations period starts when parties commit to purchase or sell).

[7] The margin of error for these estimates, calculated at the standard 95 percent confidence level, is ±5.5 percent for the first and ±3.9 for the second. In other words, we can be 95 percent confident that the actual proportions lie somewhere between roughly 38 and 50 percent for the first estimate and between 23 and 31 percent for the second.

[8] Four of the cases in the sample of § 10(b) cases produced both an order on a motion for certification and a preliminary order approving a class settlement beyond the five-year limitations period, which explains why the numbers reported for cases falling into each category sum to 139 (42 + 97) rather than 135.

[9] See Alexander Aganin, Cornerstone Research, Securities Class Action Filings: 2013 Year in Review 3 fig.2 (2014), available at http://securities.stanford.edu/research-reports/1996-2013/Cornerstone-Research-Securities-Class-Action-Filings-2013-YIR.pdf (reporting more than 3,200 securities class action lawsuits between 1997 and 2013, an average of nearly 200 per year). The “850 cases” figure was derived by multiplying the 3,200 cases filed since 1997 by the above-reported 27 percent estimate of the proportion of cases in the 500-case sample that reached a certification order after the five-year limitations period.